Concealed carry insurance helps cover legal and financial fallout after self-defense.

If you carry a firearm, you already plan for hard days. This guide on concealed carry insurance explained draws on years of research, interviews with attorneys, and hands-on policy reviews. I will break down what it covers, what it does not, and how to choose a plan with care. Keep reading for clear, calm answers you can trust.

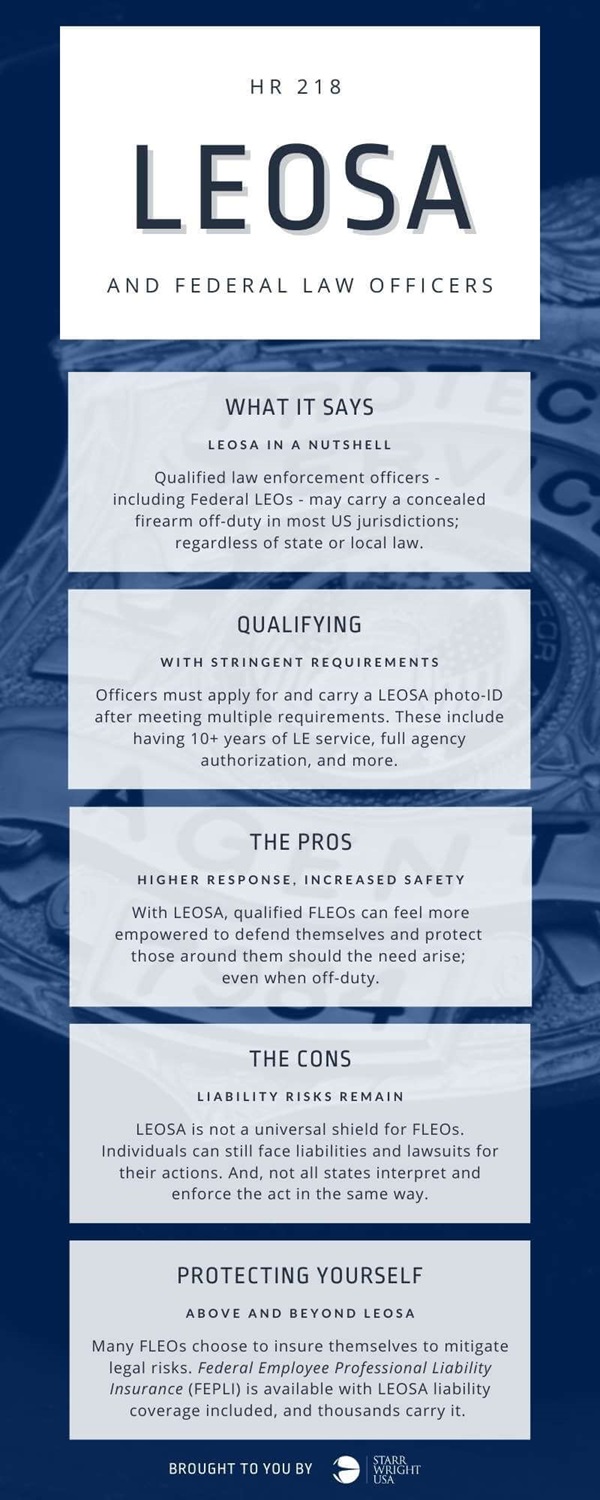

Understanding concealed carry insurance, explained

At its core, concealed carry insurance is a legal and financial safety net. It can provide funds for an attorney, bail, expert witnesses, and other costs after a lawful self-defense event. Some programs also fund civil defense and civil damages. Others add training, hotlines, and crisis support.

Concealed carry insurance explained often looks like two models. One is true insurance underwritten by an insurer. The other is a membership or legal service contract that pays for your defense. The details matter. Read how and when money is paid, what triggers coverage, and what limits apply.

Key terms to know help you compare plans with confidence. Civil defense covers lawsuits from an attacker or their estate. Criminal defense pays for a lawyer if you face charges. Bail coverage can help you get released while your case moves forward. Loss-of-earnings, counseling, and scene cleanup are sometimes included. Deductibles, per-incident limits, and exclusions set the edges of what gets paid.

Why concealed carry insurance matters

A single self-defense case can drain savings fast. Defense lawyers, experts, and investigators cost a lot. Even basic cases can run into five figures. Complex cases can climb much higher.

Concealed carry insurance explained is not a scare tactic. It is a plan for legal risk you hope to never face. Many carriers add 24/7 attorney hotlines. Some provide early attorney engagement, which may shape outcomes. The right plan can also ease stress for your family when every hour matters.

What it usually covers and what it does not

Understanding coverage lines is vital. Policies differ, but most promise help with key costs.

Common coverage areas

- Criminal defense fees when self-defense is claimed under the law.

- Civil defense for lawsuits that follow a use-of-force event.

- Bail bonds funding up to a stated limit.

- Expert witnesses, investigators, and trial support.

- Lost wages and counseling in some plans.

- Training, education, and helplines.

Typical exclusions and limits

- Acts outside self-defense, such as aggression or crime.

- Use while under the influence of drugs or alcohol.

- Unlawful possession or prohibited locations.

- Intentional wrongdoing as defined by state law.

- Brandishing, warning shots, or non-firearm force may be limited or excluded.

- Coverage may not apply in all states due to local rules.

Concealed carry insurance explained means reading the fine print. Ask how coverage applies to knives, empty-hand defense, or improvised tools. Confirm if civil damages are covered, capped, or excluded by law in your state.

Policy types and key differences

Not all plans are the same. The structure affects how fast help arrives and how secure funds are.

Major models you will see

- Insurance policies underwritten by an insurer. These function like standard lines with stated benefits and claims handling.

- Membership or legal defense networks. These are not insurance. They pay for or arrange your defense under a contract.

- Reimbursement vs. upfront payment. Some reimburse after acquittal. Others pay lawyers from day one.

- Choice of counsel. Some let you pick your lawyer. Others assign from a vetted panel.

Concealed carry insurance explained also covers state compliance. Some states limit defense coverage linked to criminal acts. That can shape how a plan is built. It can also change whether funds are paid upfront or reimbursed after charges are resolved.

![]()

Costs and how to choose a plan

Price depends on limits, benefits, and where you live. Many plans use tiered pricing. You pay more for higher limits, civil damage coverage, and extras like expert witnesses or wage replacement.

A simple checklist to compare plans

- Verify the model. Is it insurance, a service contract, or a defense fund?

- Confirm upfront payment vs. reimbursement. Ask how fast funds move.

- Check criminal and civil defense limits. Look for per-incident and aggregate caps.

- Ask about bail coverage, experts, and investigators.

- Review exclusions. Pay attention to intoxication, unlawful carry, and off-limits places.

- Look for 24/7 attorney access and response protocols.

- Read state availability and any restrictions where you live or travel.

- Scan financial strength and complaint history with regulators.

- Weigh added value. Training, courses, and real attorney seminars can be worth it.

Concealed carry insurance explained means more than price. A fair premium with clear, fast support beats a bargain with slow or uncertain help.

Real-world scenarios and lessons learned

I have sat through self-defense law classes taught by defense attorneys. I have also helped readers compare plan terms side by side. The biggest lesson is simple. Your legal fight starts the moment the event ends.

A brief example helps make it real. A licensed carrier defends against a threat in a parking lot. Police arrive. The carrier calls the 24/7 hotline and gets counsel on scene. The attorney keeps statements clear and factual. Later, a civil claim arrives. The plan pays for defense and an expert on use-of-force standards. Without coverage, those costs would sting.

Concealed carry insurance explained in practice shows common mistakes. People talk too much before counsel arrives. They assume homeowners insurance will cover them. They do not understand civil suits can follow a lawful shoot. Learn now, not later.

Laws, state rules, and compliance

Rules change by state. Some states have restricted or challenged certain self-defense insurance products. Regulators have raised concerns about policies that could appear to indemnify criminal acts. As a result, some carriers adjusted from indemnity to defense-only funding. Others pulled products from a few states.

Concealed carry insurance explained must include this caution. Always check current availability in your state before you buy. Read policy language on criminal acts, self-defense exceptions, and reimbursement. When in doubt, ask the provider for a written answer. If you travel, confirm whether your benefits follow you across state lines.

How claims work and what to do after an incident

After a self-defense incident, the clock moves fast. Your first duty is safety and aid. Then, get legal help.

Practical steps most plans expect

- Call 911. Request police and medical help. Share need-to-know facts only.

- Identify yourself to responding officers. State, “I will cooperate and I want my attorney.”

- Call the plan’s emergency hotline as soon as safe to do so.

- Avoid detailed statements until counsel is present.

- Preserve evidence if safe. Note cameras and witnesses.

- Do not discuss the event on social media.

Concealed carry insurance explained should prepare you for process. Some plans provide a response card with scripts and numbers. Store it with your permit. Train with it so you can act under stress. This is not legal advice. It is a plan to get legal advice fast.

Frequently Asked Questions of concealed carry insurance explained

Is concealed carry insurance legal in every state?

No. Some states restrict certain plan types. Check current availability and product structure in your state before you buy.

Does it cover civil lawsuits after a justified shooting?

Often, yes, but limits vary. Read whether civil defense and civil damages are covered, capped, or excluded under your plan.

Will it pay my lawyer upfront or only reimburse me?

Both models exist. Ask for written proof of how and when funds are released in concealed carry insurance explained materials.

Does homeowners insurance cover self-defense?

Usually not for criminal defense. Some policies may help with certain civil claims, but it is rare and limited.

Can I choose my own attorney?

Some plans allow it. Others require panel counsel; confirm before you enroll.

Are warning shots or brandishing covered?

Many plans exclude them or treat them as separate acts. Review exclusions for non-lethal displays and local laws.

What happens if I travel across state lines?

Coverage may follow you, but laws change by state. Verify travel coverage and any location-based exclusions.

Will my premiums rise after a claim?

It depends on the provider and product type. Some membership models keep flat fees, while insurance can re-rate.

Conclusion

You carry to protect life. Protect your future too. With concealed carry insurance explained, you can see how defense funding, attorney access, and clear limits work before you ever need them. Compare models, read exclusions, and get answers in writing. A good plan brings calm on a bad day.

Take the next step now. Review two or three plans side by side using the checklist above. Ask each provider to explain how funds move in the first 24 hours. If this guide helped, subscribe for more practical breakdowns, or leave a question so I can cover it next.